Travel

The Best Travel Insurance Companies of June 2024

Our Rankings of the Best Travel Insurance of 2024

After reviewing dozens of travel insurance providers operating throughout the U.S., the following are our top recommendations:

Our editorial team follows a comprehensive methodology for rating and reviewing travel insurance companies. Advertisers have no effect on our rankings.

The Best International Travel Insurance Companies in Detail

Learn more about each of our top travel insurance companies, including the average policy costs our team determined by examining and averaging quotes for four unique trips.

How To Choose the Best Travel Insurance

Knowing what to look for when comparing travel insurance providers can help you pick the best plan for your needs. We encourage you to compare brand pricing and policies between multiple providers to help narrow down your available coverage options.

Compare The Best Travel Insurance For International Trips

Comparing the costs of coverage offered by different providers can help you find the most affordable option for your travel insurance needs. See the table below for a direct cost comparison between the companies we’ve chosen as our top picks, as well as Better Business Bureau (BBB) ratings and notable coverage limits.

No results were found.

Asking yourself a few key questions can help further simplify your search for travel insurance. Considering the total cost of your trip, your destination, method of travel and any health concerns can help you better understand the type of policy that suits your needs best.

Was This an Important or Pricey Trip?

The value and price of your trip play a major role in travel insurance pricing. If you’re insuring a higher-value vacation, you may want to look for policies with higher overall coverage limits and travel interruption reimbursements. If you’re taking a budget vacation, you might see more value in an insurer that specializes in low-cost, affordable policies.

Where Are You Headed?

It is also good practice to consider the available amenities and your trip itinerary when shopping for coverage. For example, if you’re traveling to a remote area with a less robust medical system than a city with many options, there could be a higher chance of needing medical evacuation if you end up seriously injured. In this case, we recommend a policy with higher coverage limits on medical evacuation services.

“I recommend that every traveler gets a strong medical evacuation policy. When the worst-case scenario happens, you can get to a hospital of your choice at home. I really push this coverage for folks traveling in Mexico because it’s a short trip to a home hospital.”

How Are You Getting to Your Destination?

If you’re taking a cruise, consider getting a quote from a travel insurance provider that offers cruise-specific coverage, such as Nationwide. While most travel insurance providers design policies to cover the basic risks associated with flying — such as lost luggage, missed connections, etc. — it is worth comparing options that include coverage specific to your trip. For example, those traveling for work may prefer Allianz Global for its business-centered plans.

Do You Have Any Health Concerns?

When thinking about your travel plans, consider if you could need medical services based on your health history and travel itinerary. If you’re older, have a pre-existing health condition, or plan to participate in physical activities or sports, consider a plan with higher medical expense limits. In addition, companies often include COVID-19 treatment under a policy’s standard emergency medical coverage, but it is best to read through coverage terms and conditions to confirm.

Angela Borden, a product marketing specialist at Seven Corners, offered the following advice for travelers:

“Contact your insurance provider to be sure you fully understand the pre-existing conditions coverage for the plan you choose,” she said. “Being prepared and having the information before you need it in an emergency makes a huge difference.”

Is Travel Insurance Required?

In most cases, travel insurance is not required. However, some countries require visitors to have travel insurance due to visa requirements or diplomatic unrest. These countries typically only require proof that your policy covers emergency medical expenses. You can extend your coverage to also protect you against baggage loss, trip delays and cancellations.

Even if your destination does not mandate travel insurance, the U.S. Department of State recommends that U.S. citizens traveling overseas purchase a policy that covers unexpected medical bills while abroad.

When To Skip Travel Insurance

Travel insurance may only be worth it in some scenarios. For instance, if you booked your trip using a credit card that also offers travel insurance protection, you may not need coverage through an additional provider. We encourage you to check the details of your credit card coverage, if applicable, to ensure it aligns with your needs. If so, you can likely skip buying a separate travel insurance policy.

In addition, if you’ve booked your trip with flexible airline tickets or with a hotel that offers a flexible change or cancellation policy, you may not need a travel insurance policy. Also, travelers booking excursions or activities with refundable policies will likely not benefit from a travel insurance plan.

Finally, note that if you’re a U.S. citizen traveling within the country and have insurance through a domestic provider, you likely will need travel insurance with medical coverage. However, your coverage may not extend abroad, notably if you have a government-issued plan. But if you have private insurance that covers emergency medical expenses abroad, you may not need to purchase a travel insurance plan.

Generally, we encourage you to consider your trip, the overall cost and the flexibility surrounding your reservations when deciding whether or not to skip purchasing a travel insurance policy.

“You don’t need to insure trip expenses if they’re already covered by someone else or if you are comfortable losing the money you paid for your trip if you must cancel or interrupt it.“

What Does Travel Insurance Cover?

The specifics of what is covered under your travel insurance policy will vary depending on the provider you select. The following are some of the most common types of coverage you are likely to find as you get quotes from the best travel insurance providers.

Trip Cancellation Protection

Trip cancellation coverage compensates you for nonrefundable expenses, such as your flight and lodging, if your trip gets canceled due to certain unforeseen circumstances. This could include unexpected weather events, a death in the family or the diagnosis of a major illness. You can check your travel insurance policy for specific coverages and exclusions. Most travel insurance companies provide 100% cancellation coverage for nonrefundable expenses when offering this type of protection.

Trip Interruption Protection

Trip cancellation coverage compensates you for nonrefundable expenses, such as your flight and lodging, if your trip gets canceled due to certain unforeseen circumstances. This could include unexpected weather events, a death in the family or the diagnosis of a major illness. You can check your travel insurance policy for specific coverages and exclusions. Most travel insurance companies provide 100% cancellation coverage for nonrefundable expenses when offering this type of protection.

Trip Interruption Protection

Baggage delay or loss coverage is another component of travel insurance that offers financial protection if your checked luggage is delayed or lost during your trip. If an airline temporarily misplaces your belongings, this coverage can help ease the inconvenience by reimbursing you for essential items, such as toiletries and lost clothing. The average amount a travel insurance provider offers will vary, and some companies have a timeline for how long you must wait after a delay before you can claim this coverage.

Emergency Medical Expenses and Evacuation

Medical expense coverage is a component of travel insurance that helps you cover medical bills you incur if you get hurt or sick on a trip. Depending on the health insurance you have in the U.S., your coverage may not extend to hospital bills to treat injuries and illnesses sustained outside of the country, making this type of coverage potentially valuable in the event of a medical emergency.

Emergency medical coverage does not usually include transportation or evacuation due to an illness or injury, but concerned travelers can purchase medical evacuation insurance as an add-on. For this reason, medical evacuation protection will typically have a separate coverage limit. We recommend considering higher evacuation coverage limits if traveling to a remote area without immediate hospital access.

Cancel For Any Reason (CFAR) Coverage

Cancel for any reason (CFAR) coverage entitles you to partial or full reimbursement of nonrefundable trip expenses if you cancel your trip for reasons not listed in your policy.

“CFAR gives you greater flexibility to alter your plans and still get some money back on your trip expenses, regardless of why you decided to cancel your trip,” said Borden. “[It] was especially popular immediately after COVID-19 because it allowed people to cancel even if they simply changed their minds about traveling.”

She goes on to note that while travelers are generally less concerned about COVID-19’s impact on travel, CFAR coverage is still a valuable benefit.

“You never know what could happen at home or at your destination that would cause you to rethink your travel plans,” she added.

Collision Coverage

If you’re renting a vehicle on vacation, you may choose to add collision coverage. Similar to the collision coverage found on your domestic auto insurance policy, it compensates you for damage to a rental vehicle if you’re involved in an accident. This coverage is usually not legally required to drive in another country. Still, it may help cover repairs passed onto you by the rental car company if you’re involved in an accident.

Rental Car Coverage

Rental car agencies usually offer optional insurance coverage when you rent a vehicle. However, you could choose to opt for rental car coverage through a travel insurance plan instead. Typically offered as an add-on, it can reimburse you if a collision, theft, vandalism, natural disaster or other events damage your rental car. In some cases, you may also find it cheaper than what a rental car agency offers for protection.

What Is Not Covered by Travel Insurance?

Travel insurance will not cover everything associated with your trip. Exclusions vary from provider to provider, but companies typically omit common events and circumstances from coverage. Some examples of common exclusions include medical tourism, named hurricanes and tropical storms, and voluntary cancellation without CFAR coverage. Other standard exclusions include fear of flying, injuries resulting from participation in extreme sports and travel to particularly high-risk destinations.

Some travel insurance companies offer add-on protection plans that cover some typically excluded events. For example, CFAR coverage can partially cover cancellations not covered by your standard travel insurance policy. Extreme sports coverages or waivers can offer financial protection in the event of an injury from participation in excluded sports or activities. Regardless, we suggest thoroughly reading your contract and asking your provider questions about any exclusions you’re unsure of.

How Much Does Travel Insurance Cost?

In our comprehensive review of the travel insurance market, our team found the average cost of travel insurance was about 3% to 5% of a trip’s total value. Based on the quotes our team gathered from providers, the average cost across seven different traveler profiles came out to $221, with the average traveler paying between $70 and $300 for most trips.

To further understand the average travel insurance cost in relation to total trip value, we gathered multiple quotes from various providers for a 30-year-old traveler taking a week-long trip to France. See the table below for the average travel insurance cost based on the total cost of trips ranging from $1,000 to $10,000.

| Cost of Trip | Travel Insurance Cost | Percentage of Trip Cost |

|---|---|---|

| $1,000 | $54 | 5% |

| $2,000 | $79 | 4% |

| $3,000 | $112 | 4% |

| $4,000 | $138 | 3% |

| $5,000 | $170 | 3% |

| $8,000 | $311 | 4% |

| $10,000 | $398 | 4% |

Remember that your travel insurance costs will vary based on various factors. We encourage you to get a quote from at least three travel insurance providers before purchasing coverage to ensure you get the best price for your coverage needs.

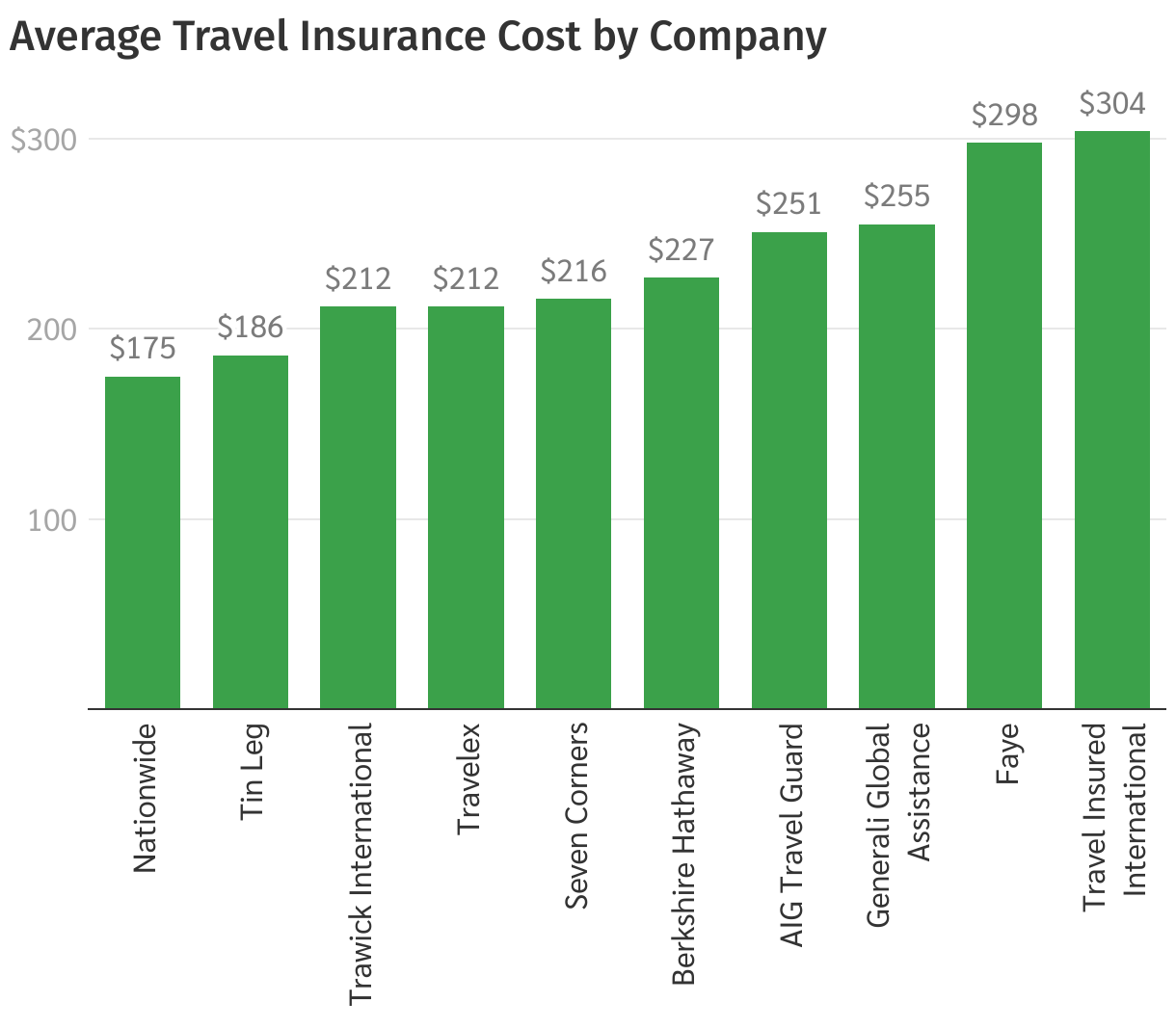

The following chart outlines the average insurance cost for our top 10 companies from least to most expensive:

We calculated the average costs for each provider in our review using seven unique traveler profiles to gain an understanding of costs for different people and scenarios, which we break down in our travel insurance methodology.

After using each profile to gather quotes for different plans, we calculated the average cost of each provider and individual policy. Our top recommended plans in the table above may cost you more or less than our averages listed depending on factors unique to your travel needs. The best way to know how much a travel insurance policy will cost is to request quotes from multiple providers for your trip.

What Impacts the Cost of Trip Insurance?

Several factors can determine how much your travel insurance will cost — and while cost matters when it comes to a travel insurance policy, the cheapest option is not always the best. If you’ve booked an expensive trip and prefer a budget travel insurance plan, it might be good to ensure the coverage is enough to protect your investment.

As you shop, keep in mind that the following factors can affect how much you pay for a travel insurance policy:

- Your age: Some travel insurance companies increase costs with traveler’s age. Based on our research, prices are the same for travelers up to age 50 and then increase from there.

- Trip cost: The more expensive the trip, the more it will cost the travel insurance company to reimburse you, according to our research. As such, your travel insurance premium will likely be higher for more expensive trips.

- Plan type: There are many different types of travel insurance policies. The more protection you have, the more expensive your travel insurance rate.

- Add-on coverages: Most plans will allow you to add certain features without upgrading your entire plan. However, add-ons will increase your overall cost. For example, you might buy basic flight insurance for $30 and add CFAR coverage for an additional $30.

- Number of travelers: While you can buy a single policy for multiple travelers, each traveler will have their own premium, increasing the total cost. However, many travel insurance companies offer group discounts.

- Destination: Your travel insurance provider will take the risk factor of your trip destination into consideration when determining the cost of insurance.

- Trip length: The longer your trip is, the more you’ll likely pay a higher premium for a travel insurance policy. Not only are longer trips more expensive, but the duration increases the chances of something going wrong and causing you to file a claim.

How To Buy Travel Insurance

The travel insurance providers on our list offer online quote systems that allow you to view pricing and policy options after entering some information about yourself and your trip. Alternatively, you can typically purchase coverage over the phone by getting in touch with a representative using the company’s customer service line.

As you prepare to purchase travel insurance, you want to keep a few details about your vacation handy, including:

- The ages and names of everyone in your party

- Your travel destination(s)

- The dates you are traveling

- Your total trip value, including flights, accommodations, baggage and other items you need to cover

- The date of your initial trip payment

Each of these factors will play a role in the price you will pay for travel insurance coverage.

Who Needs Travel Insurance?

While most people can benefit from some level of travel insurance coverage, consider a policy if you are planning any of the following:

International trips: Traveling internationally can expose you to unfamiliar healthcare systems, unpredictable events, and potential trip interruptions. Travel insurance offers financial protection for medical emergencies, trip cancellations, and unexpected expenses that may arise in foreign destinations.

Regular vacations: If you frequently travel for business or leisure, an annual travel insurance policy can be a cost-effective solution. This policy provides continuous coverage for multiple trips, saving you time purchasing separate policies.

Senior travelers: If you are a senior traveler with Medicare, your health insurance excludes most medical care outside of the country. Travel insurance with medical expenses and evacuation coverage can financially protect you if you need care while away from home.

Adventure sports: Adventure enthusiasts planning to engage in activities like hiking, skiing or scuba diving may find travel insurance with adventure sports coverage beneficial. These policies can cover potential injuries and equipment losses, which you may be more likely to run into due to your itinerary. However, not all standard travel medical insurance covers injuries related to adventure sports.

If you are considering travel insurance, we suggest getting a few sample quotes to compare coverage. Getting a quote is free, takes only a few minutes and can provide more personalized insights into the cost of your upcoming travel plan.

Travel Trends for 2024

As the world continues to recover from the impacts of the COVID-19 pandemic, the hospitality industry is slowly seeing a return to pre-pandemic levels. According to research from the U.S. Travel Association, domestic leisure travel is expected to fully return to pre-pandemic levels throughout 2024. Some of the factors contributing to travelers’ return to airports across the globe include:

- Easing international visa and travel restrictions

- Vaccine distribution and effectiveness

- Increased demand for travel following COVID-19 lockdowns

As the demand for travel increases, so has the sale of travel insurance. The travel insurance market size is estimated to grow at a compound annual growth rate of 5% between 2022 and 2028. Highly publicized stories of flight delays and cancellations occurring across the country are also contributing to public demand for travel insurance.

Top Travel Destinations of 2024

To learn more about the top travel destinations of 2024 and the average price travelers paid for coverage, our team conducted a Pollfish survey in February 2024 consisting of 1,000 U.S.-based respondents.

Of those respondents, 46% said the last time they purchased travel insurance was for a domestic trip within the U.S. The remainder of our survey participants purchased a travel policy for an international vacation, with the following countries ranking among the most popular destinations:

Is Travel Insurance Worth It?

While travel insurance is not required to enter countries in most parts of the world, it can be worth the cost to purchase some level of coverage. In our review, we found the average cost of travel insurance is less than 7% of what you can expect to pay for your vacation — but may provide hundreds of thousands of dollars in reimbursements if you experience an unexpected cancellation or delay. The medical expense coverage included with travel insurance is also an invaluable protection, as many health insurance policies exclude care provided outside of the U.S.

“Like any insurance policy, it’s a lost cost until you really need it. Travel insurance offers narrow or broad range coverages that can really help when things don’t go as planned. From Medical Evacuations to trip cancellation, it’s worth investing in a policy.”

Survey Majority Say Travel Insurance Is Worth It

Over half of our survey respondents paid between $50 to $200 for their most recent travel insurance policy, with $200 to $300 being the second most commonly selected price range. In addition, 40% of respondents said they purchased travel insurance mainly to protect the cost of their trip. Trip cancellation coverage and medical were the next most popular reasons for buying a policy.

If you plan to travel in 2024, our team recommends purchasing a comprehensive travel insurance policy. Over 60% of survey participants agree with our sentiments, endorsing a policy that includes coverage for medical emergencies, trip cancellations, baggage and more.

Ask an Expert

ASK THE EXPERTS: What is most important to consider when evaluating travel insurance options?

“It’s essential the plans are well-defined,…

including specific activities and regions a traveler will visit. For instance, a vacation spent relaxing at a nearby resort requires different insurance coverage compared to a trip involving various activities across multiple countries. Insurance premiums are inherently linked to the level of risk involved, so it’s wise for budget travelers to tailor their insurance based on their detailed travel plans.

Moreover, the inherent risks of the destination must be considered. Higher-risk areas naturally have a greater likelihood of issues arising, and appropriate insurance should be in place to manage these risks. When assessing the risk factors of a destination, it’s crucial to go beyond common knowledge and actively seek out information to accurately gauge the safety level of the destination.“

Wookjae Heo, Ph.D

Assistant Professor

School of Hospitality and Tourism Management at Purdue University

“It’s important to understand what is not covered by a travel insurance policy…

Most policies will not cover man-made disasters if your trip is canceled or interrupted. Other exclusions may include acts of war, participating in dangerous activities such as extreme sports, self-harm and foreseeable events. Read the policy carefully. One alternative to standard travel insurance is cancel-for-any-reason coverage. However, the cancellation typically must occur within a preset number of days before the trip is to begin and is more expensive.”

Frequently Asked Questions About Travel Insurance

Unlike most other types of insurance, you won’t be penalized for buying your travel insurance closer to the dates you might use it. However, many travel insurance companies require that you purchase coverage within a limited time after booking your trip. Luckily, travel insurance prices do not increase as you get closer to your departure date. That being said, some options (like CFAR coverage) may only be available for a limited time before you travel.

Your travel insurance policy will expire on the date you indicate when you purchase the plan. For most travelers, this will be the final day of your vacation. Frequent travelers might also have the option to buy annual travel insurance that protects them for a year.

International travel insurance provides you with a reimbursement for nonrefundable travel expenses if you’re forced to cancel your trip or leave your destination early. In addition, it may reimburse you for travel expenses like airfare and hotel costs if you cannot claim a refund from your vendors directly.

That depends. Most travel insurance companies require canceling anywhere from 24 hours to a week or more before departure in order to be eligible for reimbursement.

Travel insurance premiums often increase as your departure date approaches, since the likelihood of last-minute interruptions or cancellations increases closer to your flight. It’s generally advisable to purchase travel insurance in advance to get access to the most favorable rates.

The most common type of travel insurance is trip cancellation and interruption coverage, which reimburses you if you’re forced to cancel your trip or go home early. These coverages are included on almost every travel insurance policy, except medical-only plans.

Methodology: Our System for Rating Travel Insurance Companies

More Travel Insurance Guides

Exploring Online Casino Gaming: A Guide to the Thrills and Strategies

The latest jobs in search marketing

Deloitte Ports and Freight Yearbook 2024: DAESCHI mid-year update | Infrastructure | Deloitte New Zealand

Dow soars more than 700 points to close at another record high

Albares reiterates Foreign Ministry recommendations to “travel safely” on holidays

Let’s take this offline: why indie fashion boutiques are back in fashion

:max_bytes(150000):strip_icc()/roundup-writereditor-loved-deals-tout-f5de51f85de145b2b1eb99cdb7b6cb84.jpg "I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping")

I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping

Military Installation Job Fairs: Setting Realistic Expectations for Veterans

Shooting at Baltimore’s Westside Shopping Center leaves man dead, two injured