Bussiness

Recession Alert: Play Defense While Earning Up To 10% Yield

Warchi

Co-authored with Hidden Opportunities

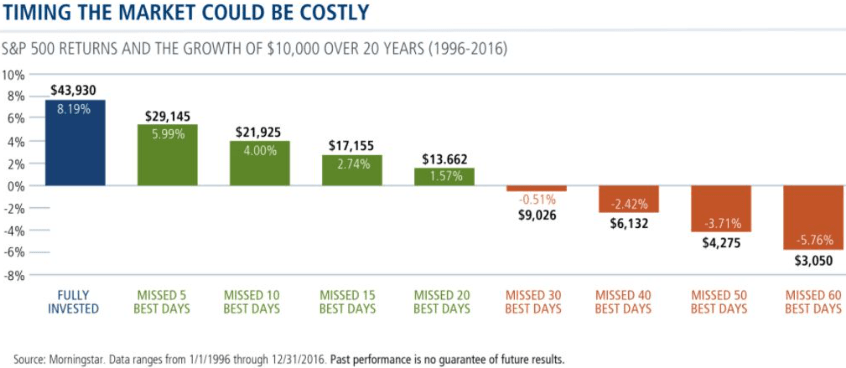

The word recession immediately makes investors uneasy and anxious, giving them the urge to sell everything and sit with cash to wait for a favorable entry point. Research suggests timing the market is extremely difficult for the average investor and will likely cause you more harm than good.

Over the last century, the stock market has faced numerous recessions and “end-of-the-world” economic conditions. But during this period, it has been the source of incredible wealth and the general trend has followed the U.S. economy towards upward growth. If you simply held through every selloff, correction, and bear market, you would’ve done incredibly well.

Timing the market to sell before the drop and buy before the recovery is really hard for the average investor to do successfully. Even if you manage to sell at the right time, the odds are high that you will miss the rally, and having cash on the sidelines will really hurt your long-term returns.

Morningstar

The unemployment rate is one of the best measures to determine whether we are in a recession at a given time. Historically, unemployment has spiked during, not before, a recession. So, the unemployment rate climbing to +4% should be interpreted as a warning sign that a recession might be happening right now.

I will be honest, neither can I time the market, nor am I interested in trying. I can’t control market sentiment or prices. This is why I follow the Income Method, to control what is controllable – my portfolio income. By staying invested in dividend payers, I keep collecting income and regularly reinvest a healthy portion to take advantage of lower prices from market crashes. My focus is on sectors that will continue to see steady demand despite economic weakness, and in this article, we discuss two picks that produce income from non-discretionary sectors – telecom and healthcare. Let’s dive in!

Pick #1: AT&T – Yield 5.9%

In four out of the last five bear markets since 1990, the telecom sector has outperformed the broader market index, with the Dot-com crash being the exception. There are only three major providers of wireless telecom services in the U.S., and these have over 90% market share. It is a very capital-intensive business to start up from scratch, not to mention significant regulatory barriers to entry. In the rapidly evolving digital ecosystem, this sector provides an indispensable service.

Whether you are applying for a job, streaming your favorite TV show, ordering dinner from your favorite restaurant, or reading this article, you are utilizing the services of this sector. Each year passes, and you evolve into a bigger consumer with more connected devices, time spent, and bills paid.

Yes, bills. A report from November 2023 found that the average American now spends $1,342 per year on their phone bill, up 5% YoY, crossing the psychological barrier of $100/month. Telecom firms in the U.S. have a robust moat and are well-positioned to benefit from increased spending on data and devices. As an investor in this sector, you can draw large qualified dividends from their predictably growing free cash flows.

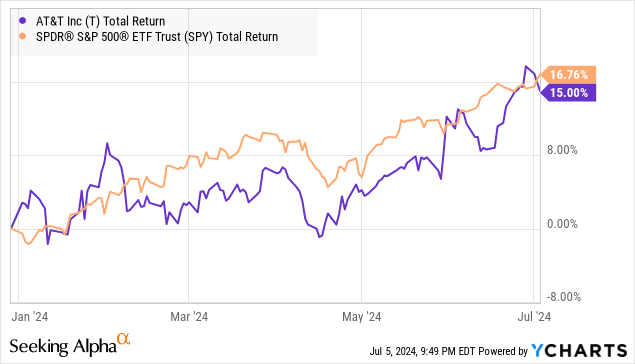

2024 is the year of FCF growth for telecom giants, after years of heavy spending on 5G and fiber rollouts. While the spending continues, AT&T (T) and Verizon (VZ) are past the peak, and their investments are bearing fruit. As such, AT&T stock has had a pleasant year so far, delivering total returns that match the popular market index while delivering usable cash in the form of qualified dividends into our accounts.

The most interesting aspect of this performance is that the company has executed exactly what it has been clearly outlining all along. The opportunity to ride the cash flow wave is far from over. The stock currently trades at a 7.9x forward PE, presenting a bargain in this richly valued market.

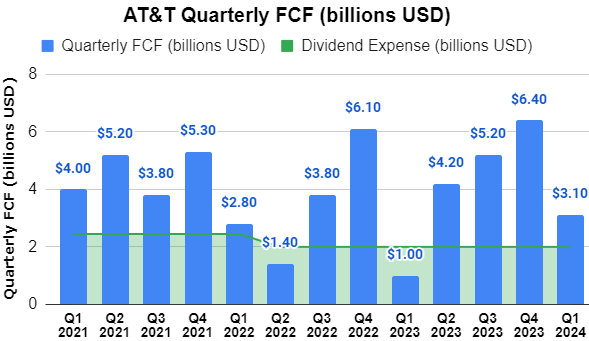

During Q1 2024, AT&T reported $3.1 billion in FCF, and has reaffirmed their full-year guidance of $17-18 billion. This places the company’s projected $8 billion annual common dividend spend at a comfortable 45% payout ratio.

Author’s Calculations

The company’s Q1 net income (after accounting for preferred dividends) of $3.39 billion placed its quarterly dividend at a 59% payout ratio. For the fiscal year, management has guided adj. EPS between $2.15 – $2.25/share, improving the dividend payout to 50%.

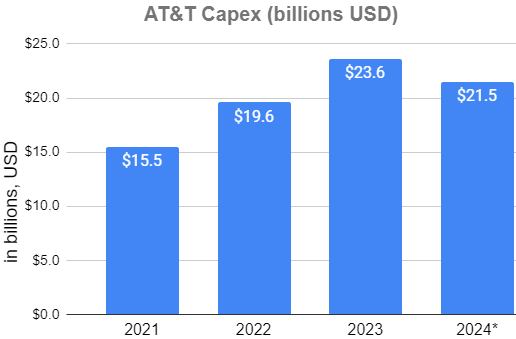

FY 2023 was the telecom giant’s peak Capex year, and AT&T expects to spend between $21-22 billion in FY 2024.

Author’s Calculations

With respect to debt, AT&T reported a weighted average interest rate of 4.2% for Q1, and much of the company’s borrowings with about 5% of its total long-term debt maturing within a year. The company is on track to bring down its debt to 2.5x EBITDA by 1H 2025. Based on these projections of lower debt, higher FCF, and lower Capex, we find the company’s current dividend to be safe and well-positioned for a healthy raise next year. We get to see all those financial and transformational improvements while collecting our well-covered 5.9% qualified yield.

Pick #2: THQ – Yield 10.6%

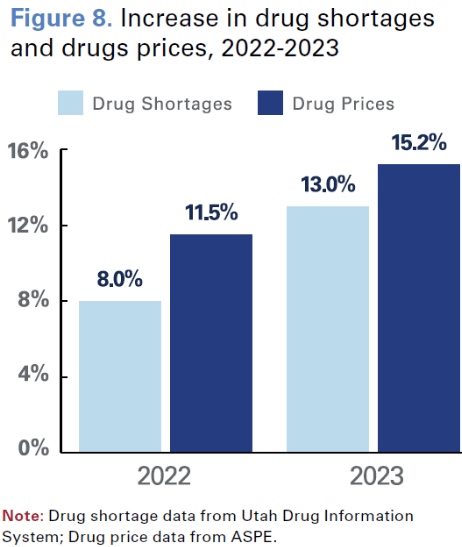

Inflation in healthcare costs, procedures, and prescription drugs in the United States has historically outpaced inflation in the rest of the economy. In 2023, dozens of leading pharma companies raised prices well above inflation. Last year, the median annual list price for a new drug was $300,000, a 35% YoY increase. According to a report by the HHS Assistant Secretary for Planning and Evaluation (ASPE), in 2022-23, the prices for nearly 2,000 drugs increased faster than the rate of general inflation, with an average price hike of 15.2%. This was further aggravated by the fact that several of the same drugs faced significant shortages. Source

AHA Website

Healthcare is one of the industries where inflationary pressure is passed to the customer without much impact on demand. Nor is the industry vulnerable to recessions. Healthcare continues to be a significant financial hurdle for most Americans, and investing in the established leaders in the sector makes a steady-long term investment.

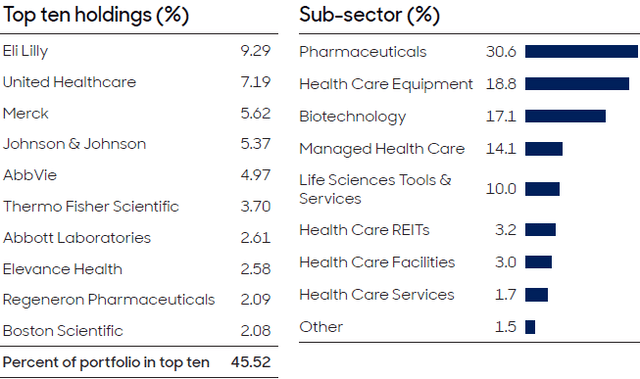

abrdn Healthcare Opportunities Fund (THQ) provided diversified exposure to leading American pharmaceutical, equipment, and biotechnology companies in the United States.

Lately, injectable medication for weight management has become highly popular. It helps adults with Type-2 Diabetes, obesity, and other weight-related problems. Eli Lilly (LLY) recently received FDA approval for Zepbound, which puts it in an excellent position to compete with Novo Nordisk’s blockbuster appetite suppressant Wegovy. LLY stock has jumped over 80% in the past year, and THQ, being an actively managed CEF, is benefitting from its strategic allocation. Source

THQ Fact Sheet

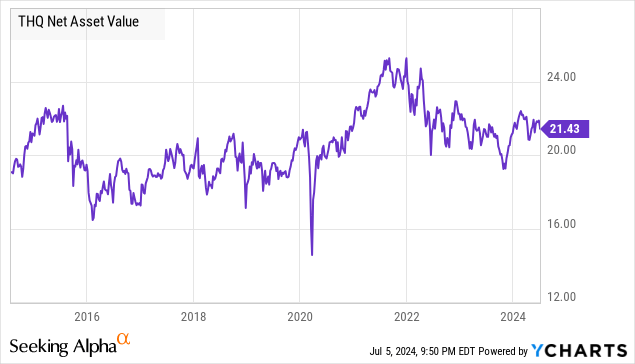

The CEF’s top ten positions are dominant in the U.S. healthcare system and represent ~45.5% of the fund’s assets. THQ pays $0.18/share on a monthly basis, a 10.6% annualized yield. THQ’s managers have done a terrific job of preserving the fund’s NAV since its inception in 2014, and we expect strong returns to continue as its new custodianship has changed to abrdn with the same team of experts.

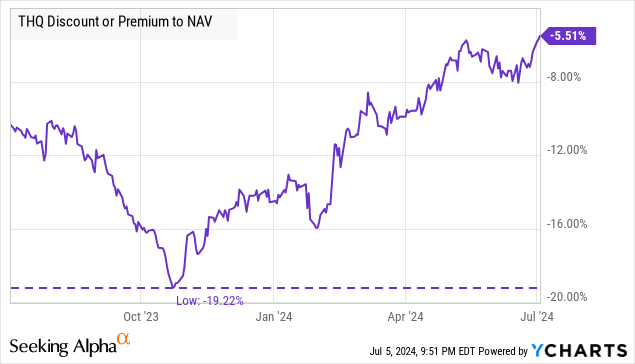

THQ trades at a 5.5% discount to NAV, and we don’t expect this to last very long. The discount has already shrunk quite a bit since Fall 2023, accelerated by the CEF’s recent 60% distribution raise.

This recently raised distribution positions THQ for a valuation upside to match or exceed that of sister CEF abrdn World Healthcare Fund (THW), which has consistently commanded a premium valuation due to the high yield, portfolio composition, and managers’ reputations and track records. Due to THQ’s focus on U.S. healthcare firms, we expect it to command a better valuation than THW over the longer term.

Healthcare is a difficult industry to understand and invest in for those who are within or related to the field. Investing in THQ provides access to the best opportunities in this lucrative field while letting the experts do the research.

Conclusion

“Well if I had just sold right there and bought right here. I would’ve avoided the whole downturn and made a lot of money.” – every other average investor.

Hindsight is always 20/20, but it’s never crystal clear at the inception of a real market crash.

“Far more money has been lost by investors in preparing for corrections, or anticipating corrections, than has been lost in the corrections themselves.” – Peter Lynch, investor, mutual fund manager, and author.

Amidst market uncertainty, we are focusing on defensive sectors like utilities, telecom, healthcare, and fixed-income securities, and we are boosting our positions accordingly. Our model portfolio holds over 45 picks targeting a +9% overall yield, implementing the strategy we fondly call the Income Method. As income investors, time in the market is money in our pockets; we get paid to stay invested through market volatility. By concentrating on steady dividend income from a diversified portfolio, we seek winning returns, recession or no recession. This is the beauty of income investing.

Exploring Online Casino Gaming: A Guide to the Thrills and Strategies

The latest jobs in search marketing

Deloitte Ports and Freight Yearbook 2024: DAESCHI mid-year update | Infrastructure | Deloitte New Zealand

Dow soars more than 700 points to close at another record high

Albares reiterates Foreign Ministry recommendations to “travel safely” on holidays

Let’s take this offline: why indie fashion boutiques are back in fashion

:max_bytes(150000):strip_icc()/roundup-writereditor-loved-deals-tout-f5de51f85de145b2b1eb99cdb7b6cb84.jpg "I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping")

I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping

Military Installation Job Fairs: Setting Realistic Expectations for Veterans

Shooting at Baltimore’s Westside Shopping Center leaves man dead, two injured