Bussiness

NVIDIA Corporation Just Beat Earnings Expectations: Here’s What Analysts Think Will Happen Next

As you might know, NVIDIA Corporation (NASDAQ:NVDA) just kicked off its latest quarterly results with some very strong numbers. NVIDIA beat earnings, with revenues hitting US$26b, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 15%. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for NVIDIA

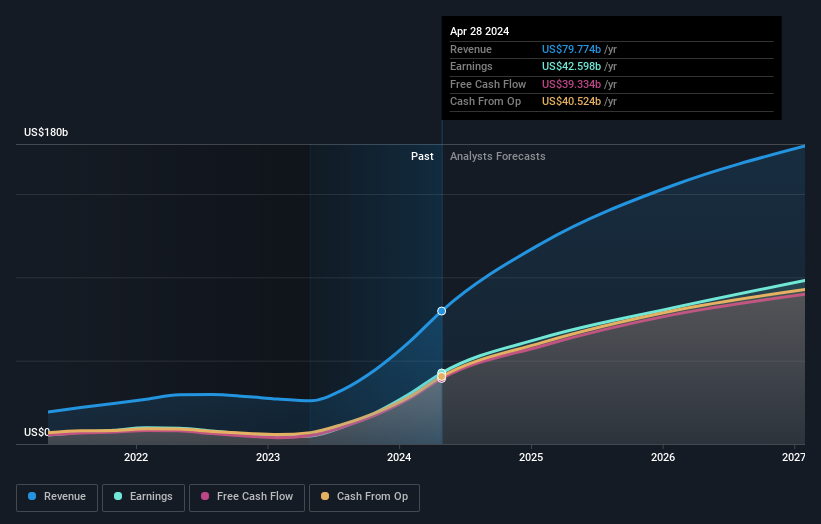

Taking into account the latest results, the consensus forecast from NVIDIA’s 53 analysts is for revenues of US$120.5b in 2025. This reflects a substantial 51% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to shoot up 48% to US$25.57. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$112.8b and earnings per share (EPS) of US$23.21 in 2025. So it seems there’s been a definite increase in optimism about NVIDIA’s future following the latest results, with a nice increase in the earnings per share forecasts in particular.

With these upgrades, we’re not surprised to see that the analysts have lifted their price target 14% to US$1,166per share. There’s another way to think about price targets though, and that’s to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on NVIDIA, with the most bullish analyst valuing it at US$1,400 and the most bearish at US$754 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await NVIDIA shareholders.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting NVIDIA’s growth to accelerate, with the forecast 73% annualised growth to the end of 2025 ranking favourably alongside historical growth of 37% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 17% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect NVIDIA to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around NVIDIA’s earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn’t be too quick to come to a conclusion on NVIDIA. Long-term earnings power is much more important than next year’s profits. At Simply Wall St, we have a full range of analyst estimates for NVIDIA going out to 2027, and you can see them free on our platform here..

Don’t forget that there may still be risks. For instance, we’ve identified 1 warning sign for NVIDIA that you should be aware of.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Exploring Online Casino Gaming: A Guide to the Thrills and Strategies

The latest jobs in search marketing

Deloitte Ports and Freight Yearbook 2024: DAESCHI mid-year update | Infrastructure | Deloitte New Zealand

Dow soars more than 700 points to close at another record high

Albares reiterates Foreign Ministry recommendations to “travel safely” on holidays

Let’s take this offline: why indie fashion boutiques are back in fashion

:max_bytes(150000):strip_icc()/roundup-writereditor-loved-deals-tout-f5de51f85de145b2b1eb99cdb7b6cb84.jpg "I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping")

I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping

Military Installation Job Fairs: Setting Realistic Expectations for Veterans

Shooting at Baltimore’s Westside Shopping Center leaves man dead, two injured