Bussiness

If I Had To Invest $100,000 In Dividend Aristocrats

da-kuk

Written by Sam Kovacs

Introduction

Last Sunday, I published an article on Seeking Alpha titled “If I had to retire with 10 Dividend Aristocrats, it would be these“.

Author’s AI Art

Those that read the article got the point, but others leaped to the comment section to ask me: “Why on earth would you want to retire with just these 10 dividend aristocrats?”.

The answer, of course, was that I wouldn’t. For one, I’m not entirely convinced by the premise that a quarter-century of uninterrupted dividend growth is necessarily a positive signal.

One just needs to look at 3M (MMM), Walgreens Boots Alliance (WBA), and AT&T (T) over the past years to realize that even safe “Dividend Aristocrats” can tumble and crumble.

I believe that while the history of dividend growth is an important metric to consider when assessing dividend safety, it is only a secondary input.

Ability and willingness to grow the dividend come way higher in the selection process.

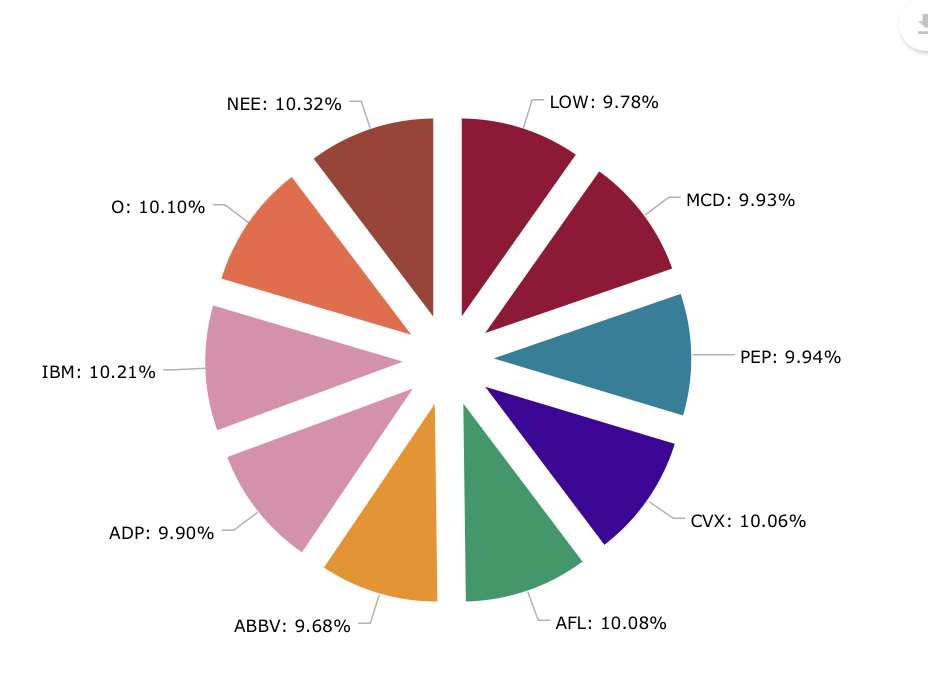

Nonetheless, the exercise of reducing the list of Dividend Aristocrats to a list of stocks that I’d be willing to buy was a good one, as it really reduced the list down to 10 picks.

- NextEra Energy (NEE)

- Lowes (LOW)

- McDonald’s (MCD)

- PepsiCo (PEP)

- Chevron (CVX)

- Aflac (AFL)

- AbbVie (ABBV)

- Automatic Data Processing (ADP)

- IBM (IBM)

- Realty Income (O)

I believed it would be of value to show you what a portfolio composed of these stocks would look like. So I created an illustrative portfolio to walk you through the process.

Portfolio Diversification

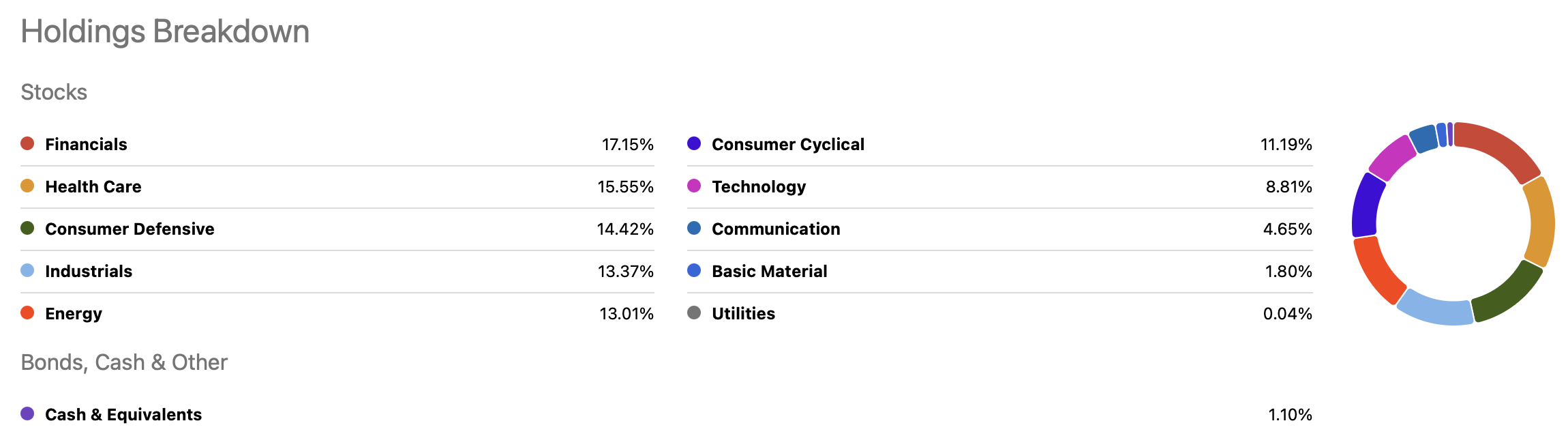

The advantage right off the bat, assuming we created a $10,000 position in each of these 10 stocks, is that you’d be rather well diversified. You’d be overweight tech and consumer discretionary, which is maybe not the tilt I’d want to have in the current market.

Furthermore, you’d lack industrials, communications, and materials exposure. Not that there is anything wrong with not being exposed to all sectors, this approach would fall short of that. By definition, we weren’t going to be able to be exposed to all 11 sectors with just 10 stocks.

Dividend Freedom Tribe

These would also be quite different from the constituents of Schwab’s US Dividend ETF (SCHD). The ETF has no utilities and no REITs. I’m sure that everyone can agree that with the Fed on track to cut rates, being underexposed to the two sectors with the highest interest rate sensitivity might be an oversight.

SeekingAlpha

But my problems with such a portfolio don’t come from owning only 10 stocks. While I prefer to own more than 10, thinking 30 is a good minimum amount for investors to own, and personally favoring the 40-70 range, I can concede that if picked with extreme care, a 10 stock portfolio could work.

No, my bigger problems come from the dividend potential of such a portfolio.

Dividend Profile

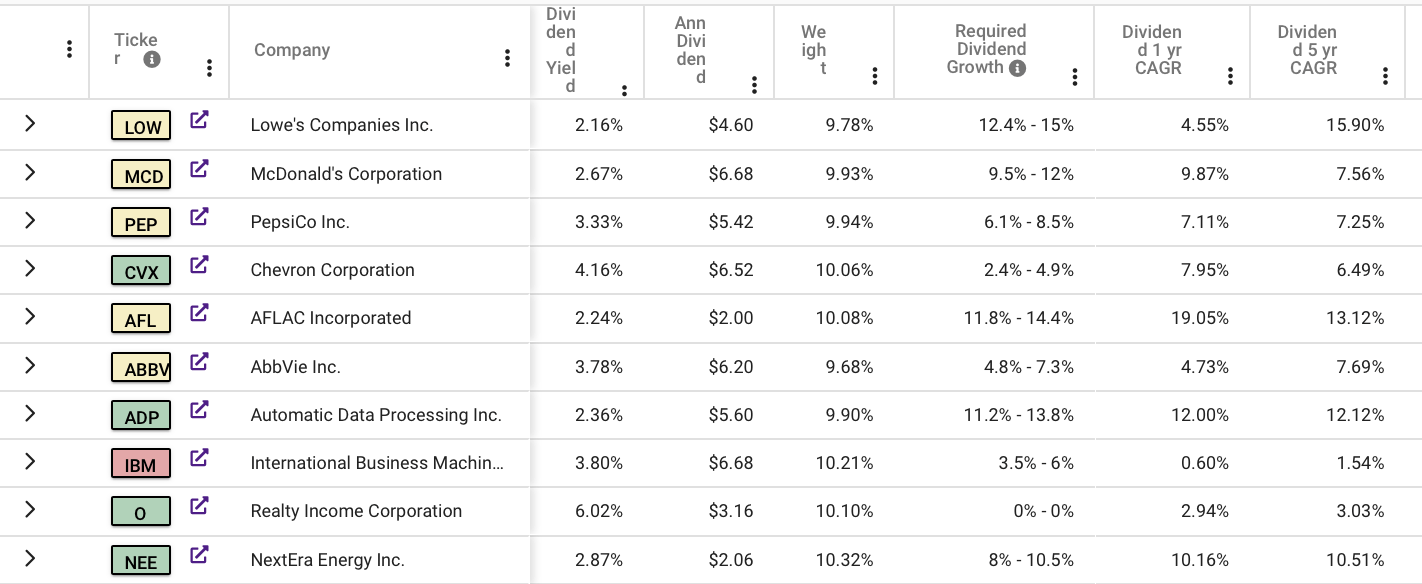

In the table below, you’ll see for each of these stocks whether I consider that they are a “Buy” a “Hold” or a “Sell” based on the color coding of the labels.

This is in part the issue for me if someone was hell-bent on buying 10 dividend aristocrats at current prices. For the most part, they’d be doing so while investing in stocks which are not at attractive prices to buy.

Dividend Freedom Tribe

As a reminder, my framework is quite straightforward:

- There are prices at which a stock is undervalued, relative to peers, fundamentals, and importantly its dividend profile.

- There are prices at which a stock is overvalued, and should be gradually sold so that you can reinvest in other undervalued names.

- There are prices where a stock should be held, or if not owned, watched.

This is the essence of our Buy Low, Sell High, Get Paid To Wait mantra.

Investors would be well served following this because as you can see the 1 year, 3 year, and 5 year dividend growth rate columns above are below my required yield on each of these positions for the most part.

If you want your dividends to snowball at an attractive pace, you need to buy stocks at the right prices.

If you ended up with this portfolio of stocks over time, waiting to buy these stocks when they were cheap, you’d probably do fine, but today’s you would get standard equity returns.

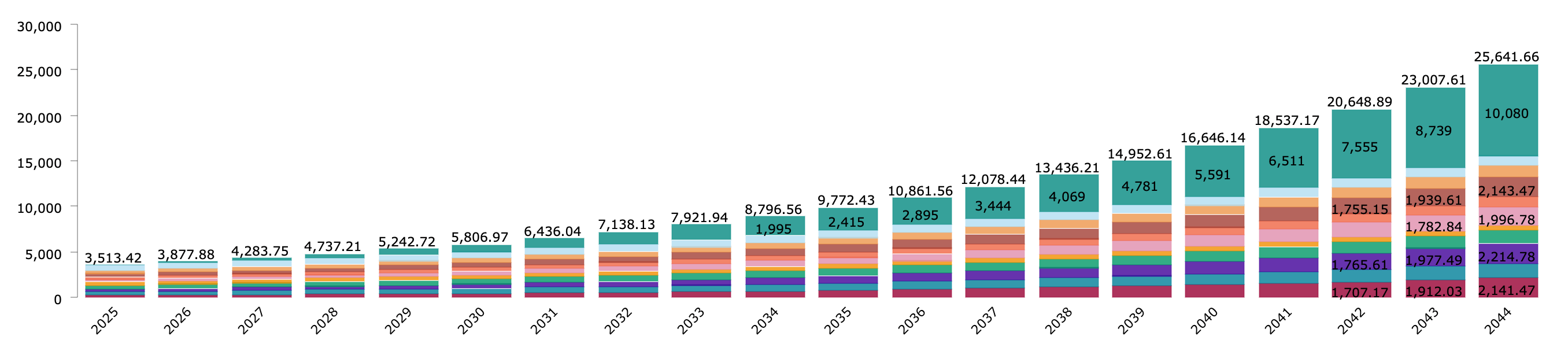

The chart below shows a 20-year income projection from this $100K portfolio.

I assumed the dividend growth rates as projected for each of the stocks in my previous article, which I copied back here for clarity:

- AFL: 12%

- ABBV: 4.5%

- ADP: 12%

- CVX: 6%

- IBM: 2%

- LOW: 12%

- MCD: 7.5%

- NEE: 10%

- PEP: 6.5%

- O: 3%

The portfolio has approximately a 3% yield and a 7% weighted (to the yields and weights) growth rate. So I’ll assume dividends are reinvested at that yield and growth rate.

10 years from now, the portfolio would generate $8,801 in annual income, and $25,600 annually in 20 years from now.

Dividend Freedom Tribe

This assumes no further capital contributions for simplicity.

In 10 years, therefore, the portfolio would yield 8.8% of the original investment, and after 20 years that would climb to 25.6% of the original investment.

While this beautifully demonstrates the power of compounding and shows the power of dividend reinvestment combined with diversification, I believe investors would be settling for less than they could get.

I like to see 8-10% of the original income projected in 10 years, and 25% in 20 years as a minimum target. And this portfolio passes the minimum target.

This shows how combining stocks also works. Add 6% yielding Realty income that’s growing at 3%, to 2% ADP growing at 12%, and the combined result is 4% yield growing at 5% per year.

But dividend investors who want to maximize their dividend income should take a differentiated approach.

Conclusion: Here’s what you should do instead.

The point of this article, and the previous article, was to demonstrate that Dividend Aristocrats only guarantee past success, not future success, especially if you want to do better than “good enough”.

If you want to do a lot better, one needs to take a better approach than just buying blue chips at whatever the price. A sense of timing needs to be considered.

I’ll conclude this article with how I approach markets, and how I suggest dividend investors do so:

- Don’t get attached to any stock. There’s no reason to “like” companies, they serve us only as a mean to an end.

- Don’t pay too much attention to dividend history. I like to see some history of consistent dividend growth, but payout ratios, top and bottom-line growth, management’s vision all play a lot more in determining future dividends than history.

- Charlie Munger said that he would rather buy a wonderful business at a fair price than a fair business at a wonderful price. I want both. Give me the wonderful business and the wonderful price. Patience pays off with investing. Find stocks which are obviously undervalued, as you cannot change the growth rate you’ll get on your dividends, but you can change the yield, by waiting and buying at the right time. The pendulum always swings.

- Let stocks bottom out. In the quest of getting the most yield on any given stock pick, you might end up bottom fishing. This is a sucker’s move. Wait for stocks to bottom out, let them show signs of a turnaround, and of regaining momentum before initiating the position. You still get most of the gain, and nearly none of the pain.

- Hold your stocks as long as business runs as usual, growth meets your targets, and nothing suggests you should sell.

- But if your dividend stocks get extremely overvalued, it makes sense to sell them and reinvest in something undervalued. If you buy a 4% yielding stock, sell it when it yields 2% and buy another 4% yielding stock, you’ve doubled your income.

Exploring Online Casino Gaming: A Guide to the Thrills and Strategies

The latest jobs in search marketing

Deloitte Ports and Freight Yearbook 2024: DAESCHI mid-year update | Infrastructure | Deloitte New Zealand

Dow soars more than 700 points to close at another record high

Albares reiterates Foreign Ministry recommendations to “travel safely” on holidays

Let’s take this offline: why indie fashion boutiques are back in fashion

:max_bytes(150000):strip_icc()/roundup-writereditor-loved-deals-tout-f5de51f85de145b2b1eb99cdb7b6cb84.jpg "I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping")

I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping

Military Installation Job Fairs: Setting Realistic Expectations for Veterans

Shooting at Baltimore’s Westside Shopping Center leaves man dead, two injured