Infra

Applied Digital: An Alternative Way To Invest In AI Infrastructure (NASDAQ:APLD)

")

Oselote

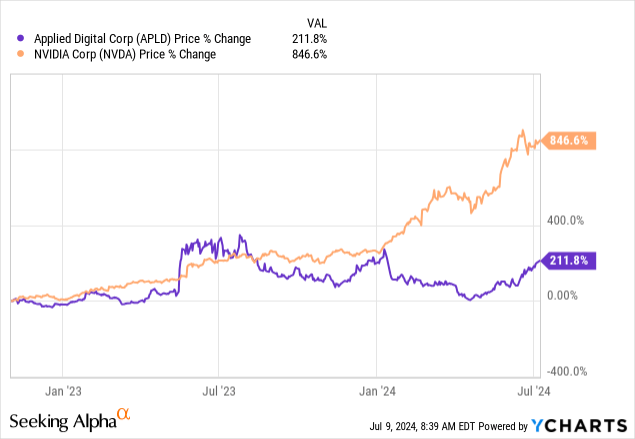

Trading at around $7, Applied Digital Corporation (NASDAQ:APLD) has surged by more than 200% since November 2022 as charted below, even outperforming Nvidia (NVDA) last year and nearly catching up at the beginning of this year before dipping. This price action could suggest some investors view the HPC (high-performance computing) data center play as an alternative way to ride the AI story.

Indeed, with Applied Digital Corporation’s greenfield approach compared to other data centers, this thesis aims to show that it should play an important role in building the infrastructure needed for AI models. These would be trained on the semiconductor giant’s sophisticated GPUs in optimal conditions.

Thus, Applied Digital Corporation stock is a buy, but, not only based on its role in the artificial intelligence value chain but also given it is undervalued, especially relative to Nvidia. First, I provide some insights into why its previous role as a blockchain hosting provider makes it particularly suitable to host AI workloads.

Shifting from Blockchain to AI Data Center

Initially known as Applied Blockchain, it changed to its new name in November 2022, coinciding with the launch of OpenAI’s ChatGPT which also clearly underlies its objective to shift to artificial intelligence. Now, there are so many players already available, like Equinix (EQIX) and Digital Realty Trust (DLR), just to name the two most significant publicly traded ones in the industry. And that is not to forget the hyperscalers like Amazon (AMZN) beefing up their internal capability. So, one may have doubts about the chances of Applied Digital competing in the space.

There are, given Nvidia is selling billions of dollars’ worth of GPUs that need to be racked in data centers as part of the AI value chain. Normally, just like the CPUs that preceded them, these GPUs are also destined for data centers. However, environmental conditions vary as an AI rack can consume double the power of conventional equipment, without forgetting the advanced cooling required for the power-hungry processors.

One way to address this challenge is to retrofit older data centers with new power bars and cooling systems, which is not the ideal solution. It is preferable to think twice before embarking on such a strategy. Furthermore, currently, most of the incumbents are concentrated in metro areas like North Virginia, where some counties have planned restrictions for data center development. In this respect, Dominion Energy (D) has seen demand increasing sharply due to the need to energize power-hungry AI workloads, which puts pressure on renewables as part of the energy mix.

On both these two constraints, Applied Digital seems to have the solution. First, with its background as a Blockchain colocation services provider used to look for cheaper renewable sources of energy throughout the U.S., it has built an AI data center (HPC hosting segment) in North Dakota. Second, this is a greenfield facility, meaning it does not have to go through the difficulties of retrofitting an old facility.

Revenue Generating but Making Losses

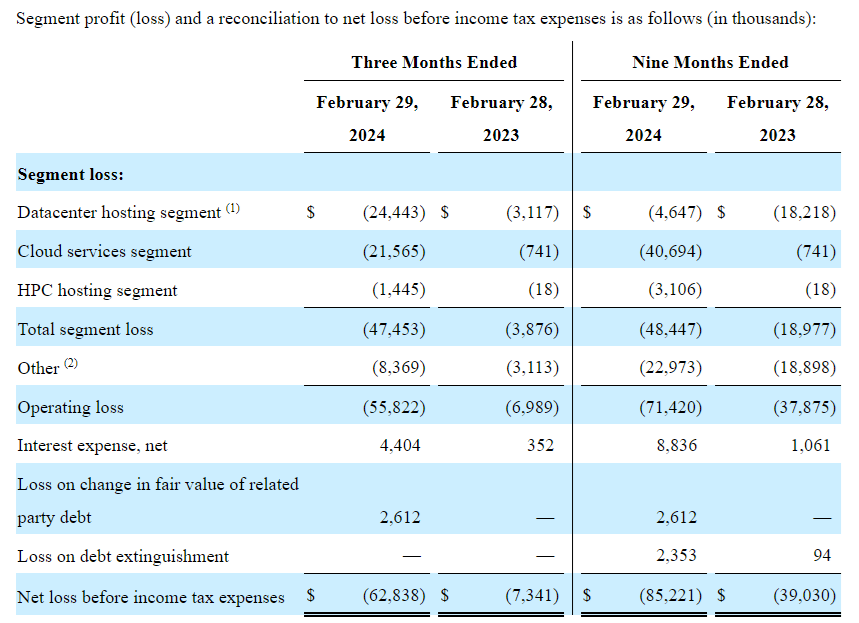

Moreover, it has an existing conventional facility (Data Center Hosting segment) which generated the bulk, or $37.8 million, out of the total $43.3 million of sales for the third quarter of 2024 (FQ3) which ended in February. The rest was made up of its Cloud Services segment, with HPC hosting not yet revenue generating.

However, this is a loss-making company as shown below, with losses being compounded by $4.5 million in revenue shortfalls by the power outage at its 180 MW data center hosting business which occurred in January.

SEC filing (seekingalpha.com)

Additionally, there were $21.7 million in losses associated with the “held-for-sale” classification Garden City blockchain mining facility. The site was sold to Marathon Digital (MARA) for $87.3 million (net purchase price) as part of diversifying away from Bitcoin to HPC, and the transaction is expected to close in the second quarter of 2024. The sale also entitles the company to $12 million of restricted cash related to the collateralized loan associated with the site.

Investing Heavily in a Rapidly Growing Gen AI Market

This also means inflows for the balance sheet, which held $290 million in net debt at the end of Q1. However, to pursue its growth initiatives in the cloud for HPC, it needs more money and this is why it secured a $200 million private debt facility including $125 million of initial commitment with $15 million already drawn.

Now, depending on whether there are any equity offerings, this way of taking debt will only increase its debt-to-equity ratio of 248% which is much higher than others that operate data center facilities as illustrated below.

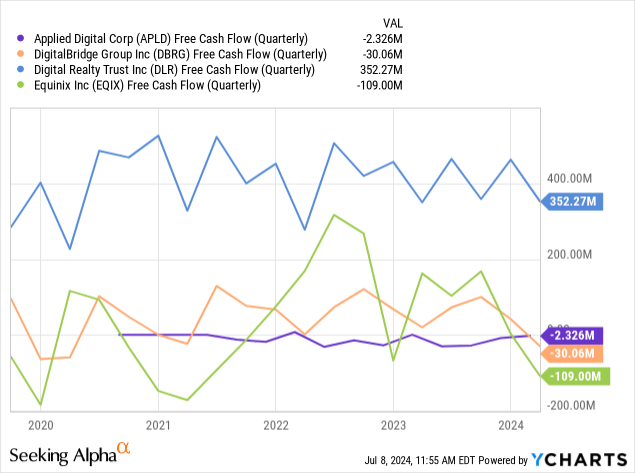

Comparison with peers APLD, EQIX, DLR, and DBRG (seekingalpha.com)

Pursuing further, for those who are used to investing in REITs specializing in data centers like Equinix and Digital Realty Trust, these have been in the industry for many years and generate higher and relatively stable cash flows from operations. For comparison purposes, I have also included DigitalBridge (DBRG) which has investments both in cell towers and data centers.

Now, only Applied Digital has a negative FCF, but, this should change as I detail later. Furthermore, the trend as per the chart below, shows that except for DLR, the free cash flows have been trending lower since the beginning of 2023, showing investments in AI.

Valuing the Company

Given the high level of investment required, Applied Digital’s approach to providing purpose-built infrastructure to take full advantage of the Gen AI market, which is expected to grow by $20 billion annually from 2023 to 2030 makes sense.

Digging deeper into cash, with the $200 million secured mortgage dedicated to HPC for the Ellendale facility I mentioned earlier, (which has been funded up to now with internal sources), the company expects to become FCF-positive this year. Soon after the financing deal on June 7, the stock rallied by around 50%, which could show market confidence in the operating model based on asset-level financing.

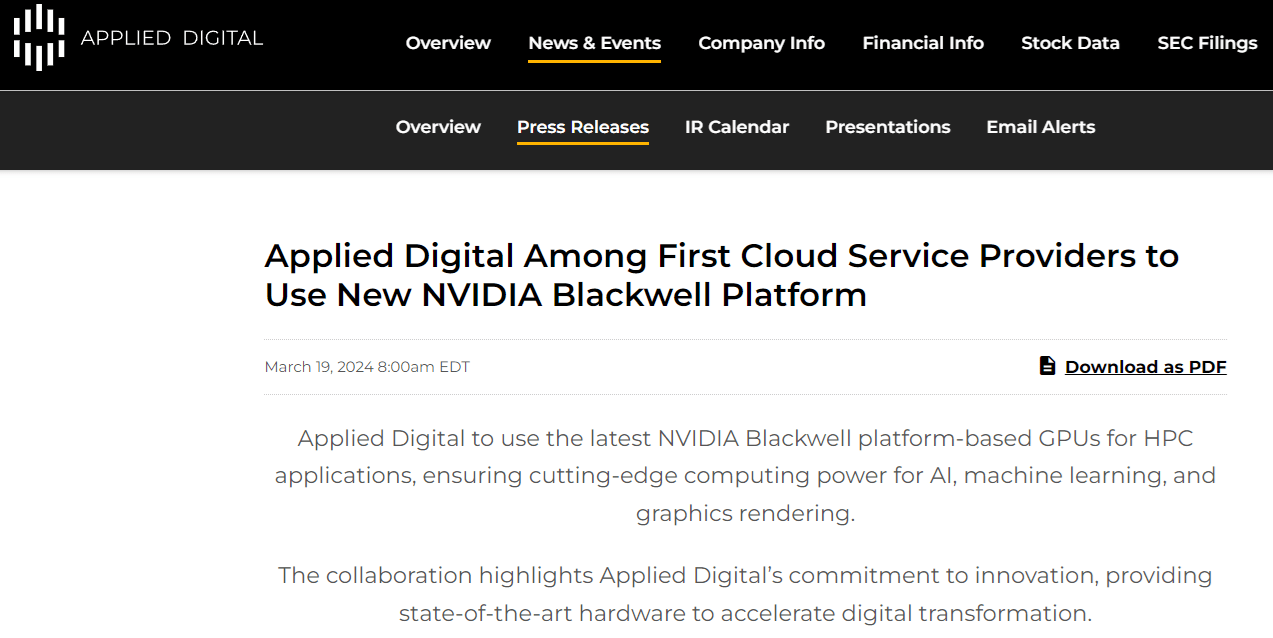

Despite the upside, its trailing price to cash flow of 18.92x is trading at a 6% discount relative to the IT sector. However, it deserves more, considering the strategic perspective, namely by positioning itself among the first cloud service providers to use Nvidia’s Blackwell platform-based GPUs for HPC applications as shown below. This approach, which consists of purchasing computing directly from Nvidia in addition to the power and cooling upfront, differentiates it from the other data center plays whose strategy consists mostly of installing GPUs on behalf of customers.

This means that for investors, Applied Digital is an alternative way of gaining exposure to the AI story compared to Nvidia, which is trading at a trailing price-to-cash flow of 49.13x. Hence, a target of 24.6x for Applied Digital, or only half of Nvidia’s due to its positioning in the AI infrastructure business, could see it undervalued by around 30% or (24.6-18.92)/18.92. Incrementing the current share price of $5.67 by 30%, I have a target of $7.4.

ir.applieddigital.com

However, this is a long-term target because of supply chain constraints and there have been some short-term setbacks that need to be highlighted.

Risks Related to Delay

First, North Dakota is far from the main supply chains of the East or West coasts, and, at a time when there is a huge AI-led demand for items like transformers used for the electrification of data centers. Thus, while the energy source is there, converting it to electricity for feeding computing equipment may take time. Second, building AI infrastructures requires specific equipment when deploying Nvidia’s complete cluster solution, which can give rise to delays. This was the case when transceivers for the InfiniBand network, a proprietary network standard for interconnecting GPU clusters, were not received in time, causing an eight-week delay in project delivery.

Furthermore, in contrast to established data centers, where the facility power is already present and revenue can be recorded as soon as the customer’s rack is energized, this is not the case for Applied Digital. This is due to starting costs or the expenses to bring facilities power online. The costs, in turn, pressured profits.

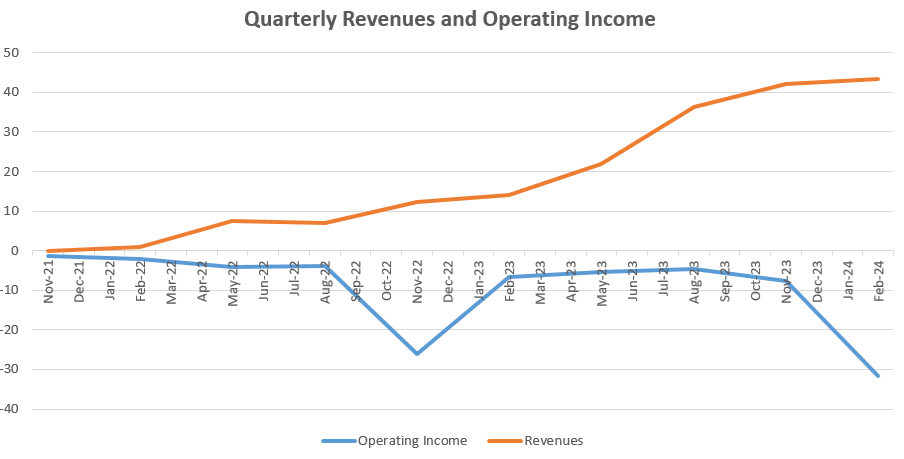

This was the case in FQ3 when the startup costs for the cloud services business were primarily responsible for additional operating expenses of $30.4 million, which was nearly a 200% increase compared to the same period last year. Therefore, depending on the execution, one may expect the same for the HPC business. Moreover, with more interest expenses related to the $200 million loan to impact the income statement, operating income may continue to trend below zero as shown in the chart below, unless revenues surge.

Charts were built using data from (seekingalpha.com)

Revenues To Surge as GPUs come Online but Amid Volatility Risks

Well, this is possible considering the eight H100 GPU clusters, which can potentially yield $20 million of annual revenue each when fully deployed. Each cluster comes with roughly 1,000 GPUs and 4,000 were already in revenue-generating mode in April with the number expected to climb to between 6,000 and 8,000 by the end of May. Now, with all 8,000 GPUs from the eight clusters online, the company could harvest $160 million for the HPC segment, resulting in boosting the overall revenues and the orange chart above rising steeply.

These revenues are coming mostly from startups and the intent is on diversifying to large enterprise customers. This diversification of the customer base to include larger enterprises is important to making sure revenues are more predictable. I believe that it can be done this year, as IT spending is expected to increase by 8% from 2023 according to Gartner. More importantly, the portion spent on data centers is anticipated to accelerate by 10% compared to 4% in 2023 led by Generative AI.

Finally, for those seeking an alternative to Nvidia, there are opportunities for Applied Digital as an emerging player in AI infrastructure and the stock could potentially appreciate by 30%. However, given the high leverage, it remains a rate-sensitive stock and was volatile on Tuesday, losing nearly 1.6% of its value. This was after the Chairman of the U.S. Central Bank, while acknowledging progress in the fight against inflation, reiterated his 2% target, which implies that interest rates will possibly stay higher for longer, or above 5%. Therefore, those investing in Applied Digital Corporation stock should be able to stomach volatility risks.

Exploring Online Casino Gaming: A Guide to the Thrills and Strategies

The latest jobs in search marketing

Deloitte Ports and Freight Yearbook 2024: DAESCHI mid-year update | Infrastructure | Deloitte New Zealand

Dow soars more than 700 points to close at another record high

Albares reiterates Foreign Ministry recommendations to “travel safely” on holidays

Let’s take this offline: why indie fashion boutiques are back in fashion

:max_bytes(150000):strip_icc()/roundup-writereditor-loved-deals-tout-f5de51f85de145b2b1eb99cdb7b6cb84.jpg "I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping")

I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping

Military Installation Job Fairs: Setting Realistic Expectations for Veterans

Shooting at Baltimore’s Westside Shopping Center leaves man dead, two injured