Bussiness

3 Reasons to Buy Nvidia Stock Before June 26

Artificial intelligence (AI) is a truly revolutionary technology that has captured the imagination of investors like few things before. This is a double-edged sword, even if the tech really is here to stay. If we learned anything from 2000, it’s that too much hype around new technology without the economics to back up sky-high valuations is dangerous territory to be in.

I don’t want to draw too close a parallel here — there are plenty of reasons to believe this is not dot-com bubble round two — but it is always prudent to maintain a healthy skepticism during a boom. All eyes — skeptics’ and believers’ alike — are on Nvidia‘s (NASDAQ: NVDA) upcoming annual shareholder meeting.

On June 26, 2024, the figurehead of the AI revolution will hold the meeting, discussing strategy and holding votes on action items like board approvals. Typically, annual general meetings don’t move the needle as much as earnings reports do, but it’s still an important event that could help shed light on what the future holds for Nvidia and the market as a whole.

So, with the meeting fast approaching, is it a good time to hop on board the Nvidia train? Here are three reasons the stock still looks strong.

1. Nvidia has a lot of cash to play with

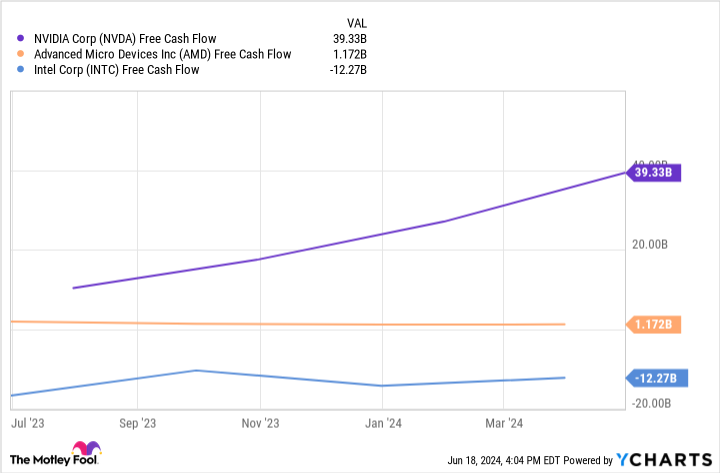

As the company has rocketed to stardom and proven how lucrative the business is, its competition wants a piece of that profit. The threat of an AMD or Intel catching up and eating into the roughly 80% market share Nvidia enjoys is real and should be taken seriously. However, Nvidia has major resources to defend itself through constant innovation.

In tech, having the best product goes a long way. AMD and Intel need to produce a product comparable to Nvidia’s if they hope to chip away at its market share. This takes money — a lot of it. AMD spent $1.5 billion in research and development (R&D) last quarter, while Nvidia spent $2.7 billion. Remember, Nvidia is already in pole position; it has the best tech on the market, and it’s still outspending AMD almost two to one.

Intel, on the other hand, is outspending both, at $4.4 billion last quarter. The catch here is that this spending is putting Intel in the red. How long can it keep it up?

Take a look at this chart showing the free cash flow (FCF) of these companies. FCF is a company’s income after you’ve subtracted operating expenses and capital expenditures (the money a company spends to grow) and it is indicative of how much headroom a company has if it wants to, say, increase R&D spending.

2. The market as a whole is growing rapidly

So if we accept that Nvidia has the resources to defend itself from its primary competitors, we can assume Nvidia can maintain or grow its market share. There are certainly more factors, but it’s not an unreasonable assumption.

Statista.com predicts a compound annual growth rate (CAGR) for the AI market at-large of about 28.5% through 2030. That is a seriously quick rate of growth, albeit slower than the lightning speed at which the company has been growing recently. Still, this would be an incredible growth rate to maintain.

This is an estimate for the entire market — not just semiconductors, which are Nvidia’s bread and butter — so this is a very rough measuring stick. The semiconductor segment could have a lower CAGR rate than this. However, this brings me to my next point.

3. Nvidia isn’t sitting on its laurels — it’s expanding its revenue streams

There’s no doubt that what has led to Nvidia’s massive success as of late is the sale of its powerful AI-enabling chips, but the company sees a future beyond this. Nvidia is attempting to build an entire AI ecosystem. It is partnering with companies like Dell to offer full-scale, on-premises, AI computing solutions. It is building technologies and end-to-end platforms designed for autonomous vehicles, humanoid robotics, and drug research. There’s more, but I’ll stop here. The point is that Nvidia intends to position itself at the very center of all things AI, as a star that other companies orbit, rather than just one more link in the chain.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $775,568!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

Johnny Rice has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short August 2024 $35 calls on Intel. The Motley Fool has a disclosure policy.

3 Reasons to Buy Nvidia Stock Before June 26 was originally published by The Motley Fool

Exploring Online Casino Gaming: A Guide to the Thrills and Strategies

The latest jobs in search marketing

Deloitte Ports and Freight Yearbook 2024: DAESCHI mid-year update | Infrastructure | Deloitte New Zealand

Dow soars more than 700 points to close at another record high

Albares reiterates Foreign Ministry recommendations to “travel safely” on holidays

Let’s take this offline: why indie fashion boutiques are back in fashion

:max_bytes(150000):strip_icc()/roundup-writereditor-loved-deals-tout-f5de51f85de145b2b1eb99cdb7b6cb84.jpg "I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping")

I’m a Travel Writer, and Out of the 5 Million Prime Day Deals on Site, These Are the 12 I’m Shopping

Military Installation Job Fairs: Setting Realistic Expectations for Veterans

Shooting at Baltimore’s Westside Shopping Center leaves man dead, two injured